Corporate tax cuts have been a contentious issue in U.S. politics since the passage of the Tax Cuts and Jobs Act in 2017. This legislation significantly reduced corporate tax rates from 35% to 21%, sparking debates about its long-term economic impact. Proponents argue that lower taxes would stimulate business investments and subsequently boost wages, while critics highlight the substantial declines in corporate tax revenue that followed. As we look ahead to 2025, the expiration of key provisions raises significant concerns about the future direction of tax legislation and its economic implications. Understanding the dynamic between corporate tax rates and the overall economy will be crucial as stakeholders navigate the upcoming tax battles.

The discussion surrounding reductions in business tax obligations has gained momentum, particularly with the upcoming expiration of provisions established in the 2017 legislation. As Congress prepares for potential reforms, alternative perspectives on tax reductions emphasize their role in influencing corporate behavior and investment decisions. The relationship between tax incentives and economic growth remains a pivotal topic, with many analysts scrutinizing how corporate tax adjustments can shape revenue and employment rates. As we approach significant decisions in the realm of fiscal policy, it becomes increasingly important to explore the various angles related to financial alleviations for corporations. The upcoming legislative changes represent a critical juncture that could redefine the landscape of corporate taxation.

The Economic Impacts of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, was heralded as a game-changing piece of legislation intended to stimulate economic growth through significant corporate tax cuts. By lowering the corporate tax rate from 35% to 21%, proponents argued that businesses would be incentivized to invest more in domestic operations, thereby creating jobs and ultimately benefiting the economy. However, economists such as Gabriel Chodorow-Reich have pointed out that while the TCJA did lead to modest increases in capital investments, the benefits did not manifest at the levels anticipated by its supporters. This discrepancy suggests that while corporate tax cuts can stimulate certain economic activities, they may not automatically translate to substantial increases in wages or comprehensive economic revitalization for the average worker.

Moreover, the analysis published in the Journal of Economic Perspectives indicates that the anticipated increases in corporate profit and ensuing wage growth fell short of projections. Instead of the predicted wage hikes in the range of $4,000 to $9,000 for full-time workers, estimates found a much smaller annual wage increase of approximately $750 per employee. This stark difference emphasizes the complexity of economic stimuli and the need for broader reform to fully realize the intended benefits of tax legislation.

Additionally, the economic landscape has been dramatically altered since the TCJA was implemented, especially in light of the pandemic. Corporate profitability soared in recent years, particularly as companies adapted to new market conditions. Chodorow-Reich’s insight into corporate tax revenues backs this up: while revenues dipped sharply in the immediate aftermath of the TCJA, they surprisingly rebounded by 2020 and even surpassed expectations. This rebound was driven by a mix of factors, including shifting supply chains and corporate adjustments to tax reporting in response to international conditions. The nuanced economic effects of these tax cuts illustrate that while immediate benefits might have seemed disjointed from their promises, longer-term analysis could yield unforeseen outcomes.

Debate on Corporate Tax Cuts: A Political Perspective

The question of whether to maintain or raise corporate tax rates in light of the findings from the TCJA remains a hotly contested issue among policymakers. Political figures are sharply divided, with some, like Vice President Kamala Harris, advocating for a return to higher corporate tax rates to fund social initiatives, while others, including former President Donald Trump, argue that further tax cuts are crucial for encouraging investment and economic growth. This split reflects a broader ideological conflict over the role of taxation in economic policy. Supporters of tax cuts claim that a lower corporate tax burden allows businesses to reinvest their earnings, thereby fueling growth, while opponents warn of the potential for reduced public revenue that can undermine essential services and infrastructure.

As Congress anticipates a brewing tax battle in 2025, the TCJA’s legacy will be central to the discourse surrounding corporate tax reform. Political narratives have already begun to shift as both parties utilize the results of Chodorow-Reich’s studies to bolster their respective arguments. The idea that corporate tax cuts might not lead to the economic dividends expected challenges the conventional wisdom embraced by many in the Republican party, prompting a reevaluation of tax legislation priorities in future discussions. The balancing act between supporting business growth and ensuring adequate tax revenue to fund government initiatives continues to be a critical discussion point, with the outcome likely influencing the economic landscape for years to come.

The Future of Corporate Taxation in America

Looking ahead, the discussion of corporate tax policy will not only focus on rates but also on the structural reforms needed to create a fairer and more effective tax system. With key provisions of the Tax Cuts and Jobs Act set to expire, there is a growing consensus among some economists and policymakers that the time has come to reevaluate the conditions under which businesses operate and how they are taxed. For instance, while reducing corporate tax rates can promote investment, relying solely on rate reductions may overlook the need for ensuring that corporations contribute fairly to federal revenues. Reintroducing certain deductions and tax credits aimed at fostering innovation and job creation could prove beneficial in the long run, as they provide targeted incentives for firms to invest in their workforce and communities.

Furthermore, the implications of shrinking corporate tax revenues necessitate careful consideration as lawmakers craft new tax legislation. The findings from the analysis by Chodorow-Reich and his colleagues indicate that not all corporate tax provisions yield the same benefits; thus, a strategic approach that balances raising statutory rates while reinstating valuable deductions could strike the right chord. This approach may not only stabilize corporate tax revenues but could also potentially enhance job creation and wage growth—aligning economic policies with social objectives. The future landscape of corporate taxation will ultimately require an interdisciplinary approach that considers economic data, political viability, and societal needs.

Re-evaluating Corporate Taxation Post-TCJA

Since the passage of the Tax Cuts and Jobs Act, the implications of structural tax reform have invited scrutiny from various angles. The effectiveness of corporate tax cuts comes into question when examining their long-term impacts on economic growth and government revenue. Researchers like Gabriel Chodorow-Reich underline that while certain provisions led to increased business investment, the overall rebound in corporate tax revenue post-TCJA illuminates a more complex relationship between tax policy and economic health than previously understood. As legislators consider adjustments in light of expiring provisions, it is vital that they analyze comprehensive data rather than rely on partisan interpretations of tax efficacy.

Moreover, with stakeholders from various sectors advocating for stability and predictability in tax policy, re-evaluating corporate taxation in the context of broader economic goals will be critical. The political discourse surrounding corporate tax cuts highlights the importance of understanding who benefits from tax reforms and how these benefits can be more equitably distributed. Ensuring that corporate taxation fosters responsible business behavior while contributing to essential public services will be vital in shaping the economic landscape for coming generations, necessitating an informed and collaborative approach between government, businesses, and the populace.

Key Provisions from the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act implemented various structural changes intended to reshape the corporate tax landscape. Key provisions included the immediate expensing of capital investments and the drastic reduction of the statutory corporate tax rate. These measures were framed as necessary adjustments to make U.S. businesses competitive in a globalized economy, where many other countries were already reducing their corporate rates. However, the implications of these provisions were not universally positive, with critics highlighting the long-term impact on tax revenues and budget deficits that could arise from such dramatic cuts to corporate tax obligations.

Another crucial aspect of the TCJA was the transition to a territorial tax system that significantly altered how U.S. companies were taxed on international earnings. By allowing businesses to repatriate offshore income at a lower tax rate, the intention was to encourage the influx of previously taxed foreign profits back into the domestic economy. The effectiveness of this change, however, has been the subject of ongoing debate, as many analysts are skeptical about whether these outcomes have lived up to their initial promises of stimulating economic growth and job creation in the United States.

Analyzing Corporate Tax Revenue Trends

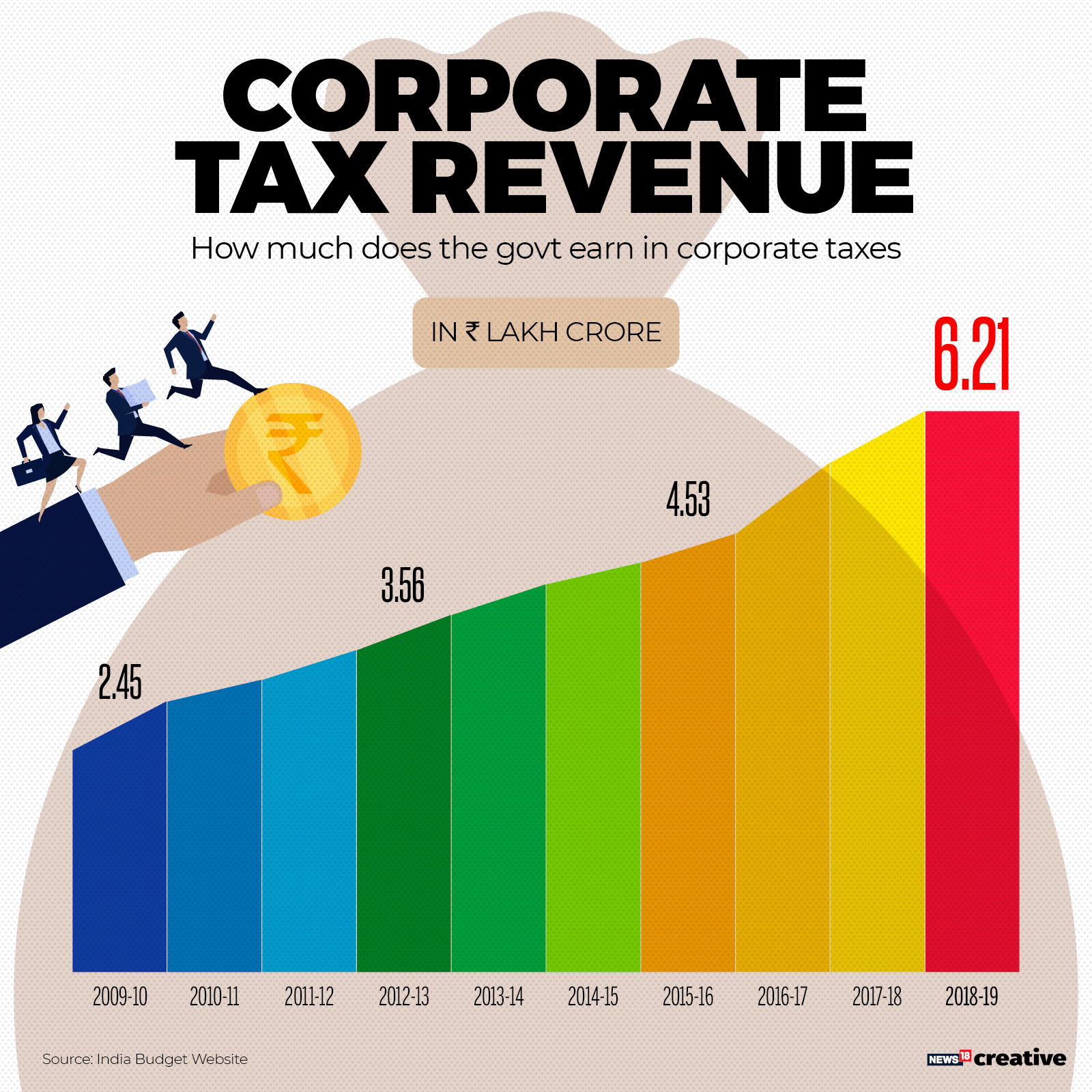

In the years following the implementation of the Tax Cuts and Jobs Act, the trajectory of corporate tax revenue saw significant fluctuations. Immediately following the tax cuts, a 40% drop in corporate revenue raised alarms regarding the implications for the federal budget. This prompted intense debates about the impact of the TCJA on government capabilities to fund essential services. However, from 2020 onward, corporate tax revenue rebounded in ways that surprised many analysts, challenging previous assumptions about the effects of corporate tax cuts on revenue generation.

This rebound in revenue, which surpassed earlier expectations, illustrated the complexities of corporate profitability and economic dynamics. Factors contributing to the surge included increased business profits tied to post-pandemic recovery, shifts in corporate tax behavior due to long-term planning, and market adaptations in response to global economic shifts. Understanding these trends will be crucial as Congress debates potential reforms in 2025, as they reflect deeper themes of resilience and adaptability in corporate behavior that policymakers must consider when crafting future tax legislation.

Implications of Corporate Tax Policy on Workforce Development

The interplay between corporate tax policy and workforce development is becoming an increasingly vital discourse as lawmakers examine the consequences of the TCJA on job creation and wage growth. The expectation that tax cuts would drive companies to hire more workers might seem logical in theory; however, recent analyses, including those by economists like Chodorow-Reich, have indicated that the actual correlation is far weaker than projected. While some investment was indeed seen in capital improvements, the anticipated direct benefit to employee compensation did not materialize to the degree that had been initially forecasted.

As Congress considers future tax legislation, lawmakers will need to address how corporate tax rates can incentivize or hinder workforce development. Maintaining lower tax liabilities without corresponding increases in wages could lead to public dissatisfaction and increased scrutiny of corporate practices. Future policy discussions should focus on creating incentives that link corporate tax responsibilities to tangible investments in human capital, ensuring that tax legislation not only promotes business growth but aligns with broader social goals, thereby fostering a more equitable economic landscape.

Corporate Tax Cuts: Misconceptions and Realities

The simplification of corporate tax cuts as a panacea for economic woes stands in stark contrast to the complex realities highlighted by the impacts of the TCJA. Advocates often espouse a narrative that unilaterally presents tax reductions as inherently beneficial for economic stimulation; however, more nuanced analyses suggest that the relationship between tax rates and economic performance is multifaceted. Chodorow-Reich’s research emphasizes that while firms do respond to tax policy changes, the overall efficacy of corporate tax cuts in driving substantial wage and investment growth is far from guaranteed.

Such misconceptions could shape public opinion and influence political campaigns as we approach 2025. The ongoing evaluations of the TCJA reveal a more tempered understanding of corporate behavior in response to tax changes, including the necessary caution required when predicting outcomes based solely on tax cut initiatives. Policymakers proposing future tax reforms must grapple with these realities, ensuring robust dialogues are rooted in empirical evidence, thus avoiding the pitfalls of oversimplified rhetoric that could misguide critical economic decisions.

Bipartisan Solutions for Future Tax Legislation

As the debate around corporate tax cuts continues to intensify, the need for bipartisan solutions has never been more pressing. While both sides of the aisle have distinct views on how corporate taxation should operate, there is common ground to be found in recognizing the necessity for a more comprehensive approach to tax reform. Empowering lawmakers to develop a blend of tax policies that focus on balancing revenue generation with incentivizing business growth could foster a more conducive environment for economic stability, benefitting voters across the political spectrum.

The successful negotiation of tax policies in the past often involved careful compromise between differing perspectives on revenue needs and economic motivations. As Congress inches closer to 2025, engaging in dialogue that focuses on redefining essential aspects of corporate taxation could pave the way for innovative frameworks that prioritize long-term economic growth while addressing pressing societal issues. Given the complexity of today’s economic environment, collaborative discussions on tax reform offer an opportunity to regenerate a more equitable tax system that aligns with contemporary economic realities.

Frequently Asked Questions

What are the key features of the Tax Cuts and Jobs Act regarding corporate tax cuts?

The Tax Cuts and Jobs Act (TCJA), passed in December 2017, significantly reduced the corporate tax rate from 35% to 21%. This legislation aimed to increase business investments and stimulate growth through various incentives, including provisions allowing immediate write-offs for new capital investments and research expenses.

How did corporate tax cuts in the TCJA impact corporate tax revenue?

Following the implementation of the corporate tax cuts in the TCJA, federal corporate tax revenue experienced a substantial drop, decreasing by approximately 40%. However, revenue began to rebound starting in 2020, driven by rising business profits that surpassed expectations.

What is the economic impact of corporate tax cuts under the TCJA?

The economic impact of corporate tax cuts under the TCJA included modest gains in wages and capital investments, estimated at around 11%. However, the overall increase in wages was significantly lower than initially projected, leading to debates over the effectiveness of such tax cuts in driving broader economic benefits.

What is the debate surrounding future corporate tax rates in light of the TCJA’s expiration in 2025?

As key components of the TCJA are set to expire in 2025, there is an ongoing debate between political factions about whether to raise corporate tax rates to restore lost revenue or to continue promoting further tax cuts to stimulate economic activity. This discussion is marked by competing narratives about the benefits and drawbacks of corporate tax reductions.

How do corporate tax cuts affect business investment decisions according to economic studies?

Economic studies, including recent analyses by Gabriel Chodorow-Reich and colleagues, indicate that corporate tax cuts can influence business investment decisions. Specifically, targeted tax provisions, such as immediate expensing, have been shown to drive higher investment compared to broad rate cuts, suggesting that how tax policy is structured plays a crucial role in encouraging corporate growth.

What are some potential consequences of changing corporate tax legislation in the upcoming tax debate?

Changes in corporate tax legislation, especially with the expiration of the TCJA in 2025, could lead to adjustments in business investment strategies, shifts in corporate profits, and alterations in hiring practices. Depending on the direction lawmakers choose, these adjustments could have significant implications for overall economic growth and wages.

What challenges exist regarding the effectiveness of corporate tax cuts in the TCJA?

The effectiveness of corporate tax cuts under the TCJA remains contentious. While some proponents argue that lower rates boost investment and drive growth, studies show only modest wage increases and significant revenue losses, raising questions about the long-term benefits of such tax cuts for the economy.

| Key Points |

|---|

| Corporate tax cuts under the TCJA reduced rates from 35% to 21%, projected to lose $100-$150 billion in revenue annually for a decade. |

| Economic analysis reveals modest wage increases and business investments tied to the tax cuts, but these were not substantial enough to counter tax revenue losses. |

| Corporate income rose initially but dropped 40% post-TCJA; however, it rebounded exceeding expectations by 2020 due to increased business profits and strategic reporting changes. |

| Chodorow-Reich emphasizes that tax cuts do not guarantee increased corporate investments and points to alternative solutions for enhanced economic effectiveness. |

| Debate continues on extending or altering TCJA provisions, highlighting a political split on corporate tax strategies between Republicans and Democrats. |

Summary

Corporate tax cuts have sparked intense discussions as lawmakers prepare for a pivotal tax battle in 2025. The Tax Cuts and Jobs Act of 2017, which significantly reduced corporate tax rates, has been scrutinized for its impact on the economy, revealing modest benefits alongside severe revenue declines. As key provisions face expiration, the discourse surrounding Corporate Tax Cuts remains vital, calling for analysis and potential reform to promote sustainable economic growth while ensuring effective tax policies.